Whether you are in or nearing retirement, you may be thinking about how your nest egg can help you achieve your financial goals in the years to come. You may also be looking to create a regular stream of income to help with retirement expenses. Now’s a good time to consider adding new tools to your retirement planning toolbelt.

One such tool is a fixed indexed annuity (FIA). With a FIA, you earn interest based in part on the upward movement of a stock market index, but you’re protected from loss if the market goes down. FIAs also give you the option to create a stream of guaranteed income that can help supplement your other income sources. Here is what to know about a FIA and how they can be beneficial as you plan your retirement strategy.

How do fixed indexed annuities work?

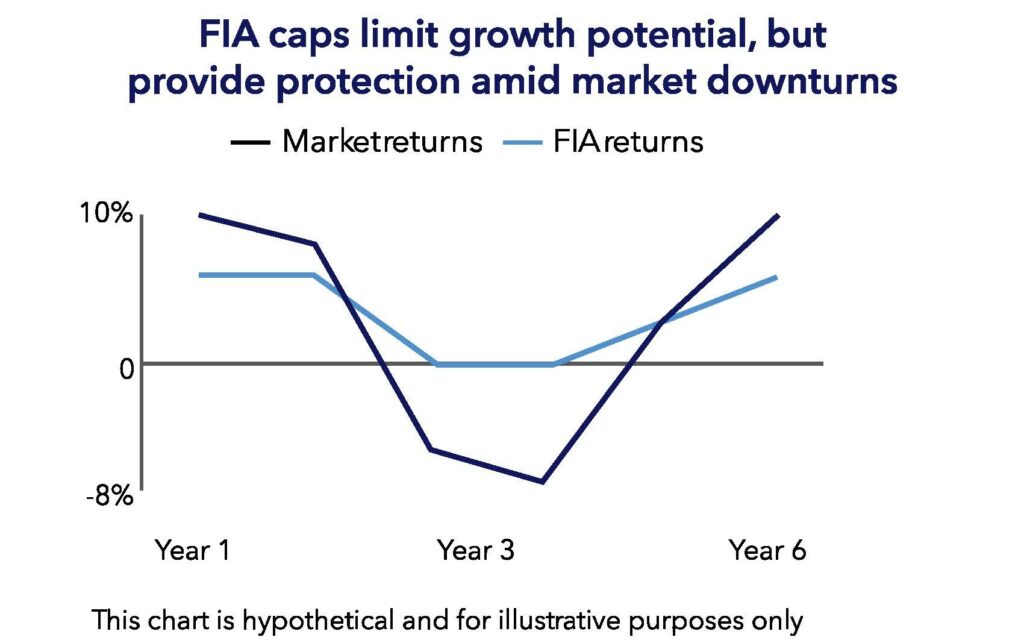

There are many types of FIAs, and each one has a unique contract and structure, but they all serve the same basic function. FIAs are a type of annuity that earn interest based in part on any upward movement in one or more reference stock market indices, such as the S&P 500®. If the net change in the index in a given crediting period is positive, then you could earn interest credits. If the net change in the index is negative, you would earn zero interest credits for that period — but never less than zero.

In order to provide that valuable protection, indexed interest credits are calculated using a formula that may include:

- A cap (an upper limit on return)

- Participation rate (the percentage of an index’s return credited to the annuity)

- A percentage-based fee, such as a spread

Why fixed indexed annuities can be ideal for retirees

One challenge in retirement is ensuring that you have enough income to cover your living expenses, for 20 years or more.

A 2022 study by Athene polled Americans on a range of retirement-related issues, including retirement savings strategies, thoughts on current market conditions, and awareness and understanding of annuities. The study found that over half of Americans (55%) are worried they will outlive their retirement savings, and two out of three consider guaranteed income an important feature when considering financial products for retirement.

A FIA can give you that stream of guaranteed income, while also helping you diversify and mitigate portfolio risk. It’s important to remember that a FIA is not an investment product. Instead, a fixed indexed annuity is an insurance product designed for long-term retirement savings that can create a “retirement paycheck” to help supplement your other income sources, such as Social Security, pensions, 401(k)/IRAs and personal assets. Plus, you have the potential to grow your income amount over time, while protecting any gains from market volatility due to market downturns.

As you consider which new tools to add to your retirement arsenal, it’s important to understand potential downsides. One consideration for FIAs is that you may not earn interest in the event of a market slump. However, you also won’t lose your principal due to market decreases, and you won’t lose any interest credits you gained while the market was up. Talking through “what ifs” with your financial professional can help you determine how a FIA might fit into your portfolio.

4 important things to know about FIAs

1. Money in annuities grows tax-deferred.

You only pay tax when you receive money from your annuity.

2. FIAs can offer higher potential interest credits than fixed rate alternatives.

Fixed rate annuities have a set interest rate, regardless of how the market performs. FIAs react to the performance of an underlying index. When the market performs well, the owner of the FIA can benefit. If the market performs poorly, it is possible to earn 0% interest, but never less than zero. A FIA can continue to provide growth potential, while also serving as a risk mitigator within your portfolio.

3. Any interest you earn is locked in and can’t be lost to future market downturns.

With a FIA, any interest you earn when the market is up isn’t lost if the market goes down. The money remains locked in once the interest is credited to your account. The way interest is credited depends on the strategy you choose. These strategies use caps, participations rates, or spreads to calculate the amount of interest you earn. Understanding how interest is credited is an important step in assessing how the FIA will work within your portfolio. Charges (for a rider, for example) can reduce the accumulated value.

4. Optional riders can offer guaranteed income, an enhanced death benefit or liquidity options.

Many consumers appreciate the customizability of a FIA. Riders can provide additional benefits, like guaranteed income or a legacy, that can help you reach your financial goals. Riders are optional elements of the FIA. These can include guaranteed income (regardless of index performance,) a death benefit that would be paid out to your beneficiary in the event you pass away before the end of the contract, or options that allow you to tap the FIA for liquidity if needed. Riders can help ensure that the FIA helps you best navigate your retirement income plan.

Is a fixed indexed annuity a smart part of your retirement plan?

“Planning for a secure retirement requires a personalized approach, so it is important for financial professionals and their clients to consider savings vehicles that can provide growth and protection for both present and future financial needs,” says Mike Downing, Chief Operating Officer for Athene.

FIAs are versatile financial products that can help you feel more confident about your financial future and better prepared for life’s uncertainties. Explore if a FIA is right for your risk tolerance, goals and the lifestyle you hope to enjoy in retirement by speaking with your financial professional. Your financial professional can also help guide you through the range of modern FIA options, help you understand and compare different products, and help you navigate which riders may be most appropriate for your situation. Since the key to a confident retirement is preparation, there’s no better time than the present to start planning.

Although fixed indexed annuities offer principal protection from market downturns, the deduction of applicable charges could exceed any interest credited, resulting in the loss of principal.

Withdrawals and surrender of taxable amounts are subject to ordinary income tax, and except under certain circumstances, will be subject to an IRS penalty if taken prior to age 59½.

Under current tax law, the Internal Revenue Code already provides tax deferral to qualified money, so there is no additional tax benefit obtained by funding a qualified contract, such as an IRA, with an annuity; consider the other benefits provided by an annuity, such as lifetime income and a Death Benefit.

Any information regarding taxation contained herein is based on our understanding of current tax law, which is subject to change and differing interpretations. This information should not be relied on as tax, legal or financial advice and cannot be used by any taxpayer for the purposes of avoiding penalties under the Internal Revenue Code. We recommend that taxpayers consult with their professional tax and legal advisors for applicability to their personal circumstances.

Guarantees provided by annuities are subject to the financial strength and claims paying ability of the issuing insurance company.

Indexed annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an index nor any market-indexed annuity is comparable to a direct investment in the equity markets.

The S&P 500® Index (the “Index”) is a product of S&P Dow Jones Indices LLC or its affiliates (“S&P DJI”) and has been licensed for use by Athene Annuity and Life Company (“Athene”). S&P®, S&P 500®, US 500, The 500, iBoxx®, iTraxx® and CDX® are trademarks of S&P Global, Inc. or its affiliates (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Athene’s products are not sponsored, endorsed, sold or promoted by S&P DJI, Dow Jones, S&P, or their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the Index.

Want the most from your retirement? Get smarter with Retirement Strategies from Basta Executive Services, LLC. Your source for tips, tools and financial solutions that can help you live your best life. Contact us today.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

This article made possible by Athene. © Athene. All Rights Reserved. Edited for content.